You’ve attempted to read and understand your company’s cash statement and it doesn’t quite make sense. You’re not alone, many business owners and professionals lack a clear understanding of their company’s cash statement and generally how to analyze cash flow at their firm. Many focus on profitability without realizing that cash is what runs the business on a daily basis.

The cash statement (which became required for financial reporting in the late 1980’s after a number of respected businesses went bankrupt, despite healthy profitability) is used by savvy business owners and investors to evaluate the quality of earnings and improve decision-making.

Understanding your company’s sources and uses of cash will help you maintain healthy cash flow and understand where some crucial improvements to your business can be made.

The Three Types of Cash Flow

Looking at a cash statement reveals three types of cash flow—Operating Cash Flow (OCF), Investing Cash Flow (ICF) and Financing Cash Flow (FCF).

Understanding the three types will help you identify key sources and uses of cash—how you are funding your business and where cash is tied up. While understanding all three types is important, the most important one to evaluate is OCF, the cash your company receives or spends in its day-to-day operations.

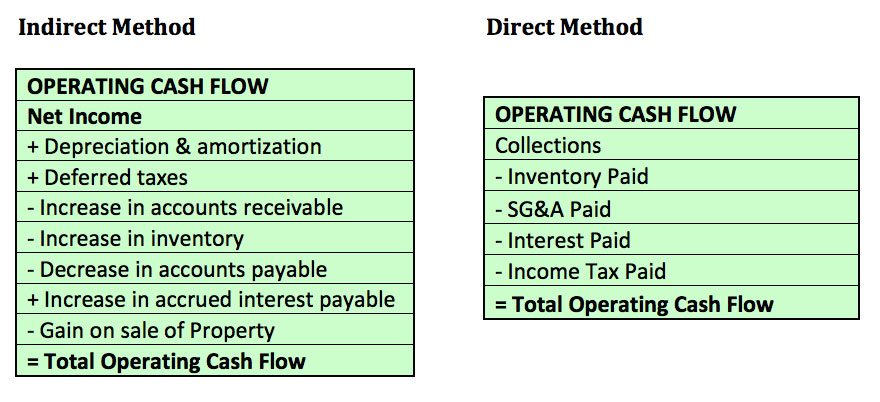

The Indirect vs. Direct Method of Cash Flow

If you took MetaMark Learning’s financial training, you are familiar with the direct method of calculating OCF. However, most companies use the indirect method, so we will provide some insight into how this method works. While the total cash flow reported remains the same under either method, what’s different is how you arrive at OCF. Investing Cash Flow and Financing Cash Flow are calculated the same under either method.

You may recall that the direct method is similar to how you track transactions in your checking account. In other words, it uses actual cash inflows and outflows to track cash from operations. Line items include cash from customers, cash paid to suppliers, taxes paid and so forth.

The indirect method, starts with net income and makes adjustments to convert this number from an accrual to a cash basis. This entails adding back non-cash items (like depreciation, amortization, or the loss on the sale of fixed assets) and adjusting for changes in non-cash current assets (such as accounts receivable, inventory, prepaid assets) and current liabilities (such as accounts payables and unearned revenue). This method is often considered easier by financial professionals because accrual information is easily accessible to calculate OCF. For non-financial professionals, the indirect method may not seem as straight forward.

The following are examples of how each method of calculating OCF might look:

Ensuring Your Cash Statement is Accurate

Regardless of the method used, it is critical that you ensure that your cash statement is accurate. In our experience, many small-to-medium sized businesses (especially those that use QuickBooks) often fail to report their Cash Statement correctly. We find that many companies struggle to setup their Cash Statement accurately from the beginning and do not take the time to fix these errors. This can result in misleading information about your cash situation.

If you aren’t sure whether your cash statement is reported correctly, we strongly encourage you to consult with a financial expert to ensure that it is accurate. Don’t have an independent one? Send your cash statement to [email protected] and we will take a look at it for free.

How to Analyze Your Statement of Cash Flows

When analyzing OCF, there are three tests that indicate how well your company is performing. You can use these tests and how they trend over a 3-5 year period to gauge the health of your cash situation.

Test #1: Is OCF Greater than Zero?

If OCF is positive, this means you can pay bills and stay in business. If OCF is negative, your operations are not generating enough cash to pay the bills, which will cause serious problems very quickly. As business owners, we all have experienced a time when cash was tight. The good news is that there is a lot you can do to make changes that can help turn a bad cash situation around (we will discuss this in more detail below).

Test #2: Is OCF Equal to or Greater than Net Income?

If OCF is greater than net income, it means your company is turning profits into cash and does not have too much cash tied up in non-cash assets such as inventory and accounts receivable. While temporary differences between cash flow and accounting-based profit are normal, problems emerge if this trend persists over time. If OCF is continuously less than net income, the quality of your earnings may be questionable and you may have a problem tying up cash needed to run your business.

Test #3: Is OCF Greater than Fixed Asset Investment (Also Called Capital Expenditures or Purchases of Property Plant and Equipment)?

If OCF is greater than fixed asset investment, it means your business is generating enough cash to fund its own growth. In other words, you do not have to borrow money or raise additional shareholder capital to make capital purchases. If it is less than fixed asset investment, then at least part of your capital investments will have to be funded from borrowing or raising additional shareholder capital.

What to do with the Results of Your Three OCF Tests

A company with strong OCF will answer yes to all three tests. Your company’s performance relative to these tests will give you a better idea of the health of your OCF. If you did not pass all three, you may be wondering what you can do to make improvements. There are a number of ways to improve OCF but the following are some of the most direct fixes:

- Plan Ahead

Regularly evaluate your company’s cash position to consider where you stand now and in the near future. Preparing good forecasts will prevent you from being blindsided by unexpected surges in expenses or numerous payments coming due at the same time.

- Assess and Renegotiate Your Payment Terms

Evaluate how quickly your customers pay you vs. how fast you are paying your bills. Before we dive into renegotiating payment terms, it is important to note that these terms play a critical role in how you manage cash flow. They are fundamental to managing receivables, inventory and payables. Lets define a couple of key terms.

Days Sales Outstanding (DSO) is the average number of days it takes to collect money owed from customers after sending them an invoice. DSO = (Average Accounts Receivable/Revenue) x 365.[1]

Days Inventory on Hand (DOH) is the number of days you can supply your customers if you stopped purchasing any new raw material. DOH = (Average Inventory/Cost of Goods Sold) x 365.

Days Payable Outstanding (DPO) is the average number of days it takes to pay money owed to vendors after receiving an invoice. DPO = (Average Accounts Payable/Cost of Goods Sold) x 365.

Now that these terms are defined, lets return to evaluating your payment terms. If, on average, you pay suppliers in 30 days but don’t receive payment from customers for 55 days, you have to float for 25 days. If it’s difficult to grasp how 25 days affects your business, do the following calculations to provide a more clear illustration of the impact:

Additional cash gained by reducing DSO 1 day = Average Accounts Receivable ÷ DSO

This number shows how much more cash you would have in your bank account by collecting receivables one day faster.

Additional cash gained by reducing DOH 1 day = Average Inventory ÷ DOH

This number shows how much more cash you would have in your bank account by reducing the amount of inventory you have by one day.

Additional cash gained by increasing DPO 1 day = Average Accounts Payable ÷ DPO

This number shows how much more cash you would have in your bank account by paying your bills one day slower. Caution: you want to be careful to balance extending payment terms without jeopardizing your relationship with suppliers.

Your accountant can provide this information and you will see how much each outstanding day costs you (and this doesn’t include the cost of short-term funding if needed during the 25 days). Then, consider renegotiating supplier and customer contract terms. You’ll have the best chance of negotiating better payment terms and discounts with strategic (key ongoing) suppliers.

Finally, be careful of early payment or bulk purchase incentives from suppliers. While the discounts may be enticing, make sure you have the cash to support your business in the interim. Many companies have gone out of business after profit-based incentives influenced the purchase of more inventory than was necessary, which tied up cash that was needed elsewhere in the business. Purchase decisions should be made or supported by someone who understands and tracks your cash position.

- Establish a Sound Collection System & Continuously Evaluate It

By putting clear systems in place to track and manage cash flow, you will have a much better chance of improving your cash situation. You’ll want to evaluate receivables, payables and inventory separately. This will help you establish better cash planning for each segment.

If your customers are not paying their bills on time, have you assigned sufficient resources to ensure timely payments (e.g., have you designated someone to oversee collections)? Are you paying your bills too fast (i.e., before they are due)? Are warehouses full of inventory that is not moving? You should be asking yourself these questions regularly to understand where cash is tied up and what actions you must take to improve cash flow and how you manage it.

- Enforce Payment Discipline & Identify and Resolve Disputes Quickly

By staying disciplined about payments, you not only improve your chances of reducing receivable days, but you give yourself a better opportunity to identify and resolve disputes with customers. The key here is communication.

Be clear about payment terms and expectations up front and train your team to recognize and address problems that arise. The best way to prevent payment disputes is to maintain good communication and have a clear process for resolving issues that may delay payment.

- Make Cash Flow a Priority at Your Company

Cash flow should be a priority at every company. If you want to get your employees on board, educate and incentivize them to understand their role in the cash cycle. This should involve employees at all levels of your business from generating sales to making a profit, turning that profit into cash and then investing that cash in expanding or improving your business. When improving cash flow is a target for everyone, interests will align to make cash flow a priority.

Finally, OCF is also enhanced by improving profitability through higher margin sales or reduced costs of sales and operating expenses. These are strategic, long-term fixes for cash flow improvement. Profitability indicates how much cash you will collect. Managing receivables, inventory and payables will tell you how fast you will collect the cash.

Conclusion

The primary purpose of analyzing your cash statement is to get a sense of the strength of your business. To see where you are generating funds, how those funds are being used and where efficiency can be improved. While profitability is important, cash is king.

Once cash flow is healthy, you can make better-informed decisions about where to use excess cash—to pay down debt, invest in a new project, distribute dividends or buy out investors. May the cash be with you!

Darrell Mullis is the Founder and Program Director at MetaMark Learning. He has over 30 years of experience teaching finance and business acumen to professionals around the world. Having worked with hundreds of companies from small local businesses to fortune 500 companies as well as co-authoring the incredibly successful book The Accounting Game™ Darrell has vast experience helping companies understand and improve financial performance and strategic thinking. Visit our website or contact us for more information about our firm and services.

[1] The number of days can be adjusted depending on the period under evaluation. For this case, we are using one year.